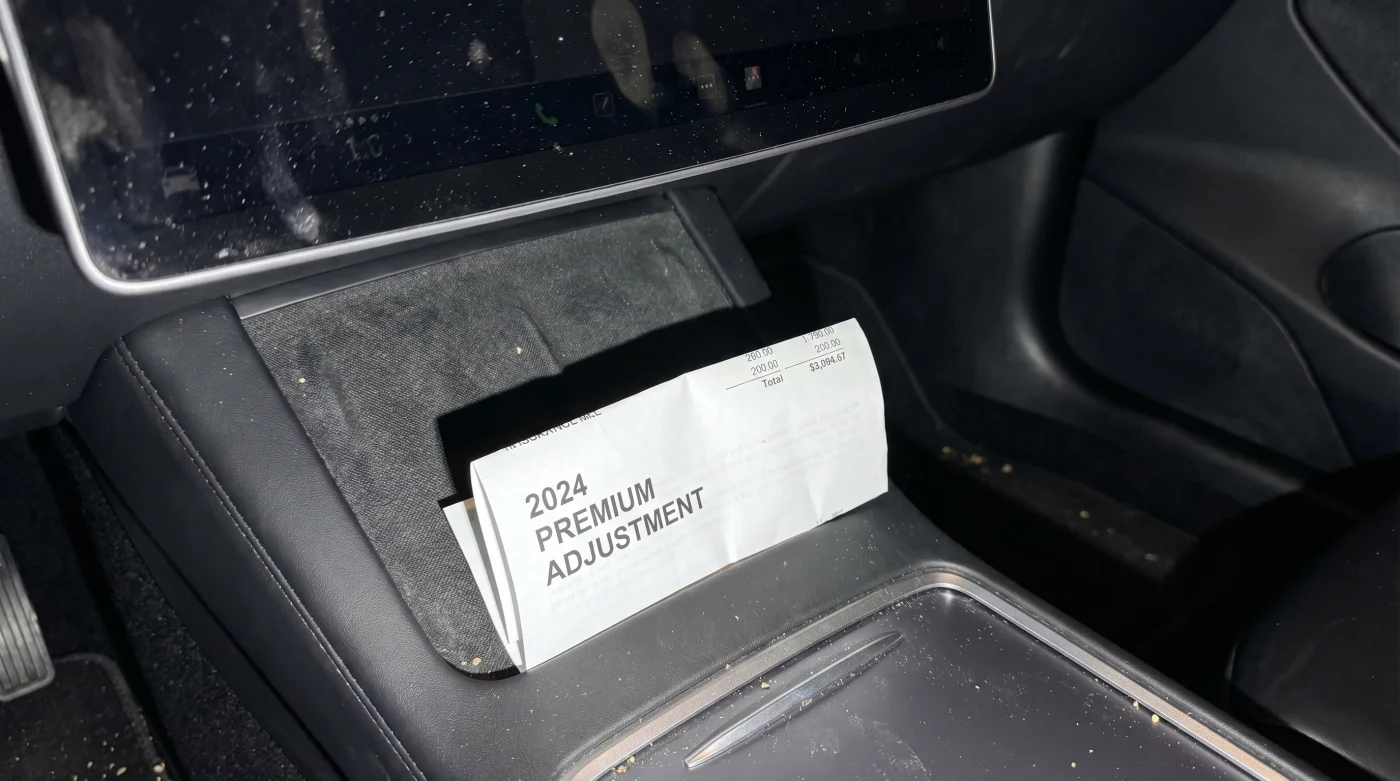

You stand by the kitchen island on a Tuesday morning, the faint smell of roasted coffee masking the stale paper scent of a freshly opened envelope. Outside, your driveway holds the sleek, silent profile of your vehicle, frost clinging to the glass in the early Pennsylvania cold. You expect the usual routine: a glance at the renewal declarations page, a resigned sigh at a marginal inflation increase, and a quick toss into the filing drawer.

But your eyes catch the bottom line, and the numbers refuse to align. The premium for your upcoming six-month cycle has not just crept up; it has surged, breaking the quiet expectation of flat-rate auto policies. You flip back a page, searching for a phantom speeding ticket or a forgotten parking lot claim, but your driving record remains as blank as the morning sky.

What you are holding is not a reflection of your driving habits. It is the fallout of a quiet, systemic shift happening across the regional insurance landscape. Major carriers operating within the state have quietly rewritten the risk profiles for this specific vehicle, reacting to internal data they prefer to keep behind closed doors.

The reality of modern ownership is shifting beneath your tires. While the public narrative praises the lack of oil changes and spark plugs, actuaries in sterile corporate offices have been tracking a different metric entirely. They are pricing in a structural flaw that contradicts standard comprehensive rates, changing the financial rules of the road.

The Perspective Shift: The Math Beneath the Glass

Most drivers treat their auto policy like a static utility bill. You pay the fee, you get the protection, and the mechanics of the agreement remain invisible. You assume that because the car lacks a highly combustible gas engine, the overall risk of catastrophic failure naturally drops over time.

Yet, the reality is entirely rooted in structural physical vulnerability. The perspective shift happens when you stop looking at your car as a collection of steel panels and start viewing it as a rolling, highly sensitive lithium-ion vault. Insurance companies no longer see a simple rear-end collision; they see the potential compromise of a unified power block running along the underbelly.

A sudden spike in battery replacement costs triggered a stealth premium hike for 2024 renewals. Carriers have realized that what used to be a minor scrape now requires a complete diagnostic teardown. If the structural housing of the battery pack shows even a millimeter of deflection from road debris, standard repair protocol dictates a full replacement, turning a minor inconvenience into a massive corporate payout.

Consider Sarah Jenkins, 44, an independent collision appraiser covering Montgomery and Bucks counties. Her job is translating bent metal into dollars. She spends her days running hands along the lower rocker panels of modern sedans, looking for the telltale signs of impact that an owner might not even notice.

It used to be about the sensors in the bumper, Sarah notes between morning inspections. But last autumn, the guidelines changed overnight. I had a client who ran over a piece of loose tire tread on the Turnpike. It slapped the bottom of the car. The casing took a localized dent. The car drove perfectly fine, but the manufacturer mandated a sixteen-thousand-dollar battery replacement to maintain safety standards. The carrier had to total the car. After a dozen of those, the underwriters panicked.

Parsing the Premium Shock

This sudden recalculation of risk does not hit every driver with the same blunt force. The carriers are applying granular, localized math, splitting drivers into distinct groups based on how and where they use their vehicles. Knowing which category you fall into is the first step in mitigating the financial damage.

If your route involves high-speed corridors like I-95 or the Blue Route, your algorithm just flagged you as a high-velocity debris risk. The actuarial tables now equate highway miles not just with standard accident risk, but with increased exposure to road hazards that threaten the undercarriage. Your policy likely reflects the steepest climb in the physical damage portion of your bill.

For the suburban leaseholder, the reality is slightly different. Because you cannot simply drop your deductibles, you are trapped in the highest bracket. The quiet rate hike here is often buried in the other-than-collision line item, masking the true cost of the battery risk underneath the paperwork.

If you own your vehicle outright and have crossed the critical threshold where the factory battery warranty expires, you face the raw edge of the market. Carriers are intensely aware that an internal cell failure might be misattributed to a road incident. Your rates are climbing because the insurance company is terrified of footing the bill for degrading hardware.

Mindful Application: Navigating the Renewal Maze

Panic is a natural reaction to a financial surprise, but clarity is the tool that solves it. You must approach the situation with a minimalist, tactical pricing mindset. You do not have to accept the printed number on the renewal page as absolute law.

You need to dissect the physical document. Open your policy side-by-side with last year’s paperwork. Look specifically at the collision line items; this is where the battery-risk padding hides.

Implement these specific adjustments to regain control over your overhead. Isolate the collision deductible first, as pushing your financial buffer higher often entirely erases the 2024 stealth hike. If you are disciplined enough to float a larger deductible in an emergency, this is your fastest lever.

- Request a structural audit: Some regional Pennsylvania carriers now offer exclusion riders for cosmetic undercarriage damage, lowering your rate if you accept the risk for non-critical scrapes.

- Shop the localized market: National mega-carriers are applying blanket rate hikes. Smaller, state-specific mutual companies often use older actuarial tables that have not yet factored in the recent spike in replacement costs.

- Verify annual mileage: Ensure your carrier is not artificially inflating your highway exposure data.

Your tactical toolkit requires patience and direct questions. When speaking to a broker, ask them specifically about their carrier battery replacement threshold. If the broker does not know what that is, you are speaking to the wrong agency.

The frustration of a higher bill is temporary, but the shift in how we manage modern transportation is permanent. You are now insuring a volatile energy grid on wheels. You are no longer just insuring a means of getting from home to the office.

Recognizing this shift brings a quiet relief. It removes the personal sting from the situation. The insurance company is not punishing your driving record; they are simply adjusting to a physical reality they failed to predict. You are caught in the growing pains of a technological transition.

True peace of mind does not come from finding the absolute lowest price. By seeing the invisible math beneath the floorboards, you take the wheel with clarity. You understand exactly what you are protecting, allowing you to drive through the Pennsylvania winter without the weight of financial uncertainty.

The future of auto coverage is not in analyzing the driver’s habits; it is in measuring the cost of a single, irreplaceable component sitting millimeters above the asphalt. — David Aris, Regional Underwriting Director

| Key Point | Detail | Added Value for the Reader |

|---|---|---|

| The 2024 Rate Spike | Carriers quietly raised premiums due to increased battery replacement costs. | Empowers you to spot the hidden fee rather than blaming your driving record. |

| Deductible Strategy | Raising collision deductibles to fifteen hundred dollars offsets the specific EV upcharge. | Provides a mathematical workaround to keep monthly expenses flat. |

| Localized Shopping | Regional mutual carriers often lack the aggressive EV risk profiles of national brands. | Directs your search toward companies actively offering fairer market rates. |

Frequently Asked Questions

Why did my specific premium jump when I have zero claims?

The increase is attached to the vehicle hardware, not your license. Carriers adjusted the baseline risk for the entire model due to statewide repair costs.Can I drop collision coverage to save money?

If you hold a loan or lease, your financier strictly prohibits this. If you own the car outright, it remains incredibly risky due to the total-loss potential of battery damage.Will a dashcam lower this specific rate hike?

While cameras prove fault in accidents, they do not lower the repair cost of the internal components. Carriers rarely offer discounts that offset structural risk.Are all insurance companies in Pennsylvania doing this?

The largest national carriers adopted these rates in late 2023. Smaller, mutual insurers are lagging behind, offering a temporary window for better pricing.How do common potholes affect my insurance standing?

Severe road impacts that dent the undercarriage shield can force a mandatory battery replacement. Claiming this turns a road hazard into a catastrophic payout on your record.