The quiet hum of the refrigerator is the only sound in the kitchen as you stare at the laptop screen. You have an extra two thousand dollars this month—maybe from a tax refund, maybe a hard-earned bonus—and the cursor hovers right over the “Additional Principal” button.

This is supposed to be the American dream in action. You chip away at the mountain, shaving months off the loan and denying the bank its unearned profit. It feels like financial rebellion, a clean, sensible victory over debt that generations before you have praised.

But the machinery behind that portal does not reward your initiative. While you are picturing a shrinking timeline and breathing a sigh of relief, the underlying algorithm is checking a completely different set of rules. The industry standard fixed-rate loan is not a static block of ice melting in the sun; it is a carefully calibrated contract.

The truth is, that satisfying click of early repayment often triggers a hidden set of financial tripwires. Your aggressive debt payoff strategy might actually be leaking money through clauses you never knew you signed, quietly sapping the very savings you thought you were securing.

Deconstructing The Yield Illusion

Imagine a massive water wheel driving an old stone mill. You think throwing a sudden, massive bucket of water at it will speed up the grinding process. Instead, the mechanism just jams, the wood groans, and a toll collector steps out to demand a fee for the spilled water. This is exactly how the banking system reacts to sudden influxes of your cash.

We are taught a remarkably simple equation from childhood: a lower balance naturally equals lower interest. But we forget that banks bundle and sell these loans based on projected, uninterrupted revenue streams. Wall Street investors rely on predictable returns, which means your early payment disrupts their tightly wound financial ecosystem.

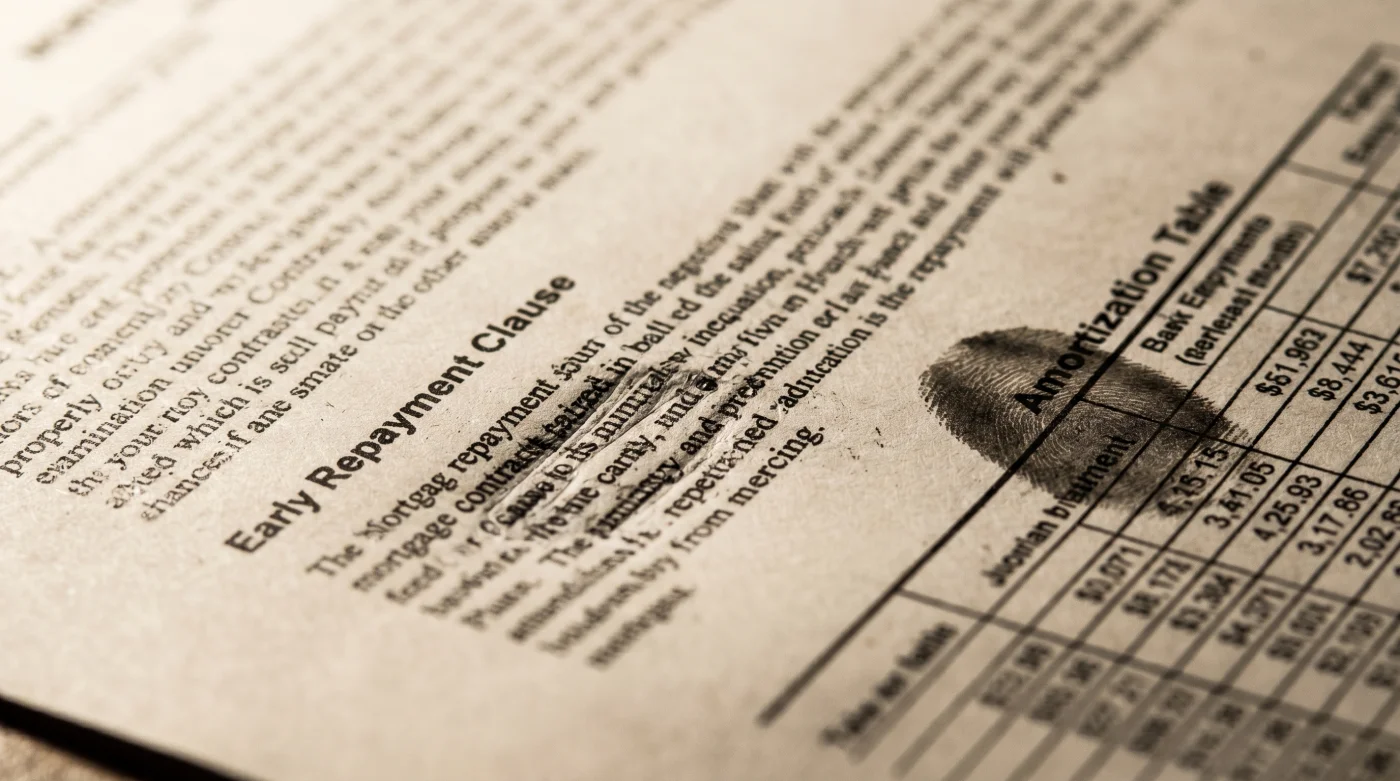

When you wipe out a chunk of principal, you are effectively breaking a promise to the bondholders who bought your debt. To protect themselves, lenders bury “yield maintenance” clauses and hard prepayment penalties deep within the amortization schedule. They ensure they get paid regardless of your thriftiness.

You are not simply returning borrowed money; you are dismantling their expected profit margin. The hidden amortization schedule algorithms automatically scan for this behavior, flagging large principal reductions and occasionally assessing a surcharge that quietly rolls into your next billing cycle.

The Architect Of The Penalty

Marcus Vance, a 48-year-old former securitization underwriter based out of Chicago, spent a decade building the exact penalty algorithms most borrowers ignore. He recalls a couple who sold a small business and threw a $150,000 lump sum at their traditional 30-year fixed loan. “They thought they were buying five years of freedom,” Marcus notes. “Instead, they hit a threshold hidden on page forty-two of their promissory note. They ended up paying an $8,000 surcharge just for the privilege of giving the bank their own money back.”

This kind of systemic friction is entirely legal and rarely discussed at the closing table. The industry standard is flawed intentionally, designed to make the borrower feel entirely in control while strictly limiting the actual speed at which they can escape the financial product.

Tailoring Your Repayment Strategy

Navigating this terrain requires shifting your focus from raw enthusiasm to calculated strikes. Depending on how your cash flow operates and how you approach your mortgage, the trap snaps shut differently.

- Synthetic Brake Fluid Quietly Deteriorates Your Older Rubber Brake Lines

- Vitamin C Serums Actively Destroy Collagen Under Artificial Office Lights

- iPhone Storage Settings Hide A Massive Background Tracking Drain

- Cast Iron Skillets Actually Rust Faster With Standard Vegetable Oil

- Merca Panama Vendors Suddenly Reject Bulk Cash Transactions Today

- TVMAX En Vivo Streaming Now Requires Hidden Hardware Upgrades

- Hyaluronic Acid Serums Double Hydration Following This Damp Towel Hack

- Microfiber Towels Scratch Car Paint When Washed With Detergent

- Stainless Steel Pans Become Nonstick Using The Water Method

- Soundbar Speakers Produce Terrible Dialogue Without This Positioning Hack

For the Aggressive Saver: You want the house paid off in ten years, not thirty. Your biggest risk is timing, specifically the hard prepayment penalty window heavily enforced in the first three to five years of the loan. Refinancing or dumping huge sums here often triggers a strict percentage fee based on the outstanding balance, erasing any interest savings you might have gained.

For the Annual Bonus Earner: You rely on a yearly lump-sum injection to make a dent in the principal. The danger here lies in how the servicer applies the funds behind the scenes.

If the payment exceeds a certain threshold, the bank might classify it as an unapproved loan modification rather than standard principal reduction. This triggers forced recasting costs or silent audit fees, turning your massive December payment into an administrative nightmare.

For the Quiet Incrementalist: You toss an extra $100 into the portal every month, hoping the drops eventually fill the bucket. The trap here is less about massive penalties and entirely about application error.

Servicers routinely misallocate these micro-payments, pushing them toward future interest or escrow buffers rather than knocking down the principal wall. You are feeding the bureaucratic beast, not starving it, simply because you didn’t check the right box.

Bypassing The Amortization Trap

Defeating this system does not require a law degree. It requires a deliberate, methodical approach to how and when you transfer your money.

You must stop treating your mortgage servicer like a high-yield savings account. Every dollar needs specific instructions attached to it, wrapped in the exact language the bank’s automated system understands.

Apply these exact protocols to shield your extra payments:

- Locate your original promissory note and search specifically for the “Prepayment” rider or “Yield Maintenance” addendum.

- Identify if you have a “soft” penalty (triggered only by refinancing) or a “hard” penalty (triggered by any large principal reduction).

- Calculate your safe harbor limit, usually restricted to 20% of the original loan balance per calendar year.

- Always use the designated “Principal Only” channel online, or write those exact words in the memo line of a physical check.

The Tactical Toolkit you need is remarkably analog. You need your Closing Disclosure (CD), a physical highlighter to mark the penalty dates, and your servicer’s online payment breakdown tab to verify the math every single month.

Timing is also a critical tool in your arsenal. Execute lump-sum payments exactly 48 hours after your regular monthly payment clears. This isolates the transaction from monthly interest accrual and forces the system to apply it purely to the remaining balance.

Securing Your True Financial Independence

The roof over your head should feel like a sanctuary, not a financial maze waiting for you to take a wrong turn. Recognizing the hidden mechanics of your fixed-rate mortgage strips away the anxiety of making the incorrect financial move.

When you understand that the system prioritizes corporate yield over your personal freedom, you stop playing their game blindly. You start directing your wealth with precision, turning a rigged contract into a predictable, entirely manageable tool for your own stability.

The ultimate relief is not just watching the balance hit zero on a screen. It is knowing you navigated the labyrinth on your own terms, protecting your capital and refusing to leave a single cent on the table for an institution that didn’t earn it.

“You cannot out-save a contract you haven’t read; the bank’s profit margin is always hidden in the fine print of your ambition.”

| Key Point | Detail | Added Value for You |

|---|---|---|

| Yield Maintenance | Banks rely on uninterrupted, predictable interest payments to satisfy bondholders. | Prevents you from accidentally triggering massive penalties when making large lump-sum payments. |

| Safe Harbor Limits | Most contracts allow up to a 20% annual principal reduction without penalty. | Allows you to confidently plan annual bonus allocations without fear of silent surcharges. |

| Payment Timing | Executing principal payments 48 hours after standard monthly clearance. | Ensures 100% of your extra cash hits the principal balance, rather than being eaten by daily interest accrual. |

Frequently Asked Questions

Is it ever safe to pay off a fixed-rate mortgage early?

Yes, provided you verify that your specific loan has passed its prepayment penalty window, which typically expires after the first three to five years.Why did my extra payment go toward next month’s interest?

Servicers default to applying extra funds to future payments unless you explicitly select the “Principal Only” option. It protects their yield.What is a soft prepayment penalty?

A soft penalty only charges you a fee if you refinance the home. You can still sell the property or pay it off with cash without being penalized.How do I find out my specific loan’s safe harbor limit?

You will find this in the “Prepayment Disclosure” section of your Closing Disclosure (CD) or the original promissory note you signed.Can I dispute a misapplied principal payment?

Absolutely. Keep your bank receipts and submit a formal “Notice of Error” to your servicer; they are legally required to correct misallocated funds.