You smooth out the edges of that crisp, thermally-printed paper ticket against the dashboard of your car. The faint smell of fresh ink mixes with the lingering scent of morning coffee. You slide it into your visor, tucking away a daydream of immediate, life-altering wealth. We all know the standard fantasy: the oversized check, the sudden deposit, the instant freedom to walk away from your desk forever.

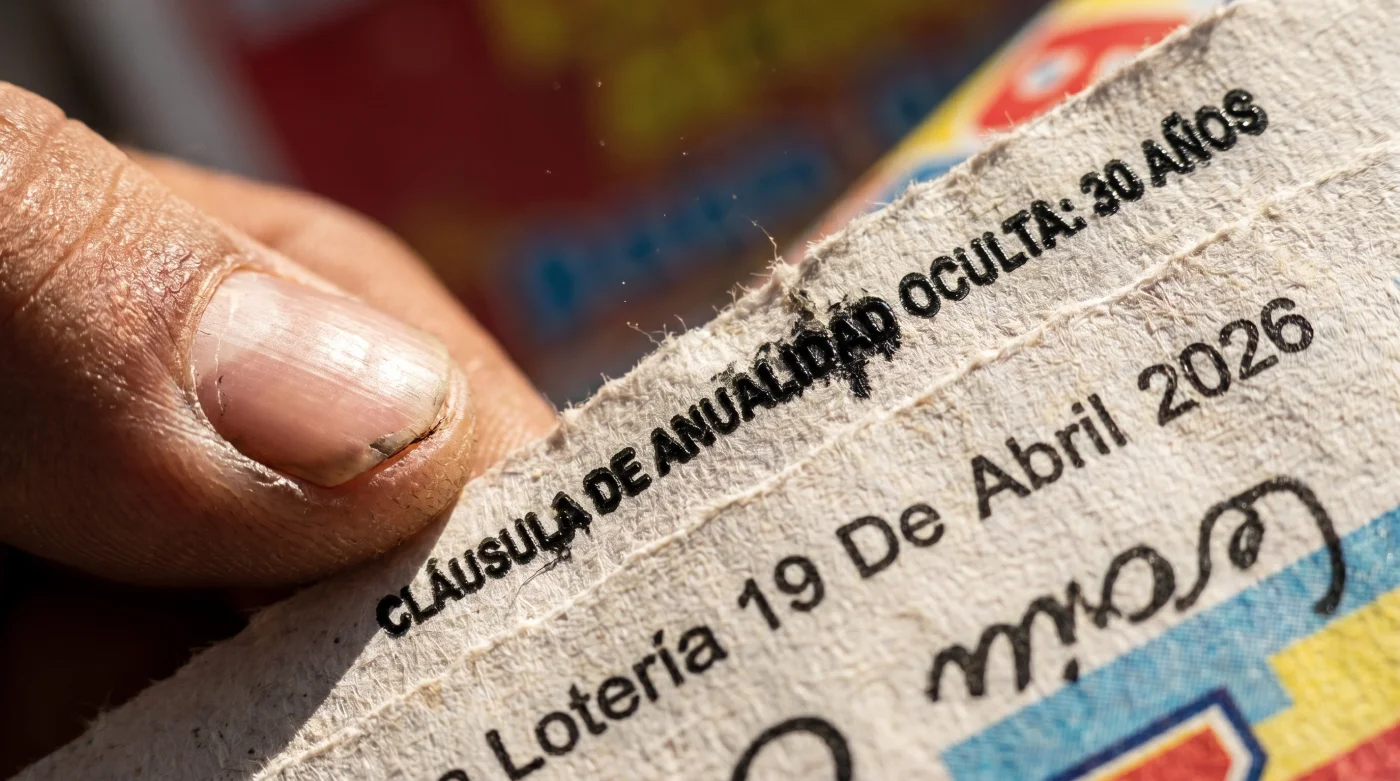

But that familiar paper slip is quietly changing its promises. If you flip over a recently printed ticket for the Loteria 19 de Abril 2026, the dense block of fine print tells a vastly different story than the draws of yesteryear. The institutional machinery behind the game has shifted the underlying payout mechanics, moving away from the loud, instant gratification we are conditioned to expect.

You might assume that holding the winning numbers means walking into a local claims office and demanding a lump-sum wire transfer by Friday. That assumption is now completely outdated. The architects behind these highly anticipated 2026 draws have rewritten the ending to your daydream, embedding a strict financial reality into every barcode.

The Hourglass Payout

Think of traditional lottery winnings like a busted fire hydrant. The pressure is immense, the volume is staggering, and without heavy equipment to control it, the water damages the very foundation it hits. The Loteria 19 de Abril 2026 introduces what industry insiders call a forced delay—a mechanism that turns the hydrant into an hourglass.

At first glance, a mandatory delayed annuity distribution feels like a penalty. You bought the ticket; you want the cash right now. Yet, when you strip away the emotional rush of the win, this hidden clause reveals itself as a profound advantage. Instead of handing you a volatile mountain of capital that attracts distant relatives and predatory investments, the system now enforces a steady, unshakeable stream of income. It protects you from the sheer shock of sudden wealth.

Marcus Thorne, a 51-year-old estate planner based in Chicago, spent the last decade trying to salvage the rapidly depleting accounts of overnight millionaires. He was reviewing the preliminary legal framework for the April 2026 draws when he spotted the subtle shift in language. ‘They did not issue a press release,’ Marcus noted, tapping his pen against the draft bylaws. ‘They simply swapped the default lump-sum clause for a staggered annuity. It is the most aggressive, quietly brilliant move to stop winners from going bankrupt.’

Adjustment Layers for the Modern Player

The way you handle this ticket must change to match the terms printed on its back. This is not just about reading the fine print; it is about recalibrating your entire approach to a potential windfall. The delayed distribution forces you to stretch your timeline and slow down your immediate reactions.

For the Pragmatist, this shift requires a new type of patience. You can no longer bank on paying off every mortgage, car loan, and outstanding debt in a single afternoon. Instead, the first year’s distribution acts as a pressure release valve, giving you enough capital to stabilize your life while the bulk of the wealth remains securely held in an untouchable, interest-bearing trust.

- Solid State Drives Outlast Newer Storage Buying This Specific Capacity

- Synthetic Motor Oil Actually Destroys Older Engine Valve Seals

- Term Life Insurance Contracts Hide A Quiet Cancellation Clause

- Stand Mixers Double Dough Capacity Using This Simple Dime Placement

- Windows 11 Diagnostic Menus Unlock Hidden Processing Power Instantly

- Honda CR-V Leather Trims Secretly Accelerate Your Vehicle Depreciation

- Baking Soda Marinades Completely Ruin Premium Steak Muscle Fibers

- Retinol Serums Nightly Applications Actually Accelerate Cellular Skin Aging

- Ligue 1 Streaming Platforms Abruptly Cancel International Viewer Subscriptions

- Everton Liverpool Match Broadcasters Suddenly Disable Mobile Streaming Access

For the Debt-Conscious, the restricted payout is actually a massive psychological relief. When you receive a lump sum, the immediate instinct is to clear all debts instantly, often ignoring the tax penalties of sudden liquidation. The staggered annuity forces you to negotiate payment plans, keeping your credit history active and preventing you from draining your initial liquidity.

For the Legacy Builder, the Loteria 19 de Abril 2026 ensures that your dependents inherit a managed system rather than a singular, depletable bank account. By stretching the capital over twenty or thirty years, the structure forces a measured pace of generosity. It guarantees that wealth outlasts the initial excitement.

Navigating the New Annuity Landscape

Preparing for this specific drawing means shifting your focus from immediate consumption to long-term management. You need a mindful, minimalist strategy to handle the bureaucratic reality of an enforced annuity. Let the noise of the lump-sum fantasy fade, and focus on the practical steps required to secure your ticket and your future.

When you purchase your tickets for the April 2026 event, treat them as delayed bearer bonds. Secure the physical slip immediately, keeping it away from heat and moisture, while mentally accepting that any payout will arrive in deliberate fractions. You must prepare for the bureaucratic waiting period before any funds clear.

The tactical toolkit for managing this new reality is remarkably simple, requiring more discipline than financial literacy.

- The 90-Day Quiet Period: Prepare to stay silent for three months post-draw. The delayed annuity means your first check will not clear immediately, giving you time to hire a fee-only fiduciary.

- The 5 Percent Rule of Thumb: Mentally allocate only a fraction of your total advertised win for first-year expenses. The new framework heavily backloads the larger distributions.

- Beneficiary Documentation: Because the payout outlives the initial excitement, you must draft a clear succession plan for the remaining annual payments should something happen to you.

- Tax Staggering: Recognize that forced annuities generally keep you out of the absolute highest single-year tax bracket, spreading the liability over a generation.

We naturally resist restrictions on things we feel we own. The idea that a lottery board can dictate how and when you receive your money feels invasive at first. Yet, this quiet pivot for the Loteria 19 de Abril 2026 fundamentally changes the nature of the game from a chaotic gamble to a structured, reliable financial instrument.

Redefining the Weight of Luck

Mastering this detail—understanding that the restriction is actually a protective boundary—gives you a rare peace of mind. It removes the paralyzing anxiety of instant wealth management. You no longer have to figure out how to invest tens of millions of dollars by Tuesday morning.

The system paces the windfall for you, allowing you to breathe, adapt, and actually enjoy the reality of your changing life. The cream should tremble at the top of your coffee, undisturbed by the rush of panic. You are no longer just a lucky winner; you are the steward of a generational timeline.

‘The restriction of an enforced annuity is the greatest invisible armor a sudden millionaire can wear.’ — Marcus Thorne, Forensic Accountant

| Key Point | Detail | Added Value for the Reader |

|---|---|---|

| Forced Annuity | Winnings are distributed annually over 20-30 years instead of a single lump sum. | Prevents the total depletion of funds within the first three years of winning. |

| Staggered Taxation | Taxes are applied only to the yearly distribution amount, not the entire jackpot. | Keeps you in a more manageable tax bracket, preserving total wealth over time. |

| Built-in Cooling Period | Initial payouts face a mandatory administrative delay of up to 90 days. | Provides crucial time to hire legal and financial counsel before the money arrives. |

Frequently Asked Questions

Is there any way to opt out of the 2026 delayed annuity clause?

No. The new terms are hardcoded into the rules of the drawing. Purchasing the ticket acts as your binding agreement to the staggered payout schedule.What happens to the remaining money if I pass away?

The balance of your annuity does not disappear. It becomes part of your estate, and the scheduled payments will transfer directly to your designated beneficiaries.Will inflation destroy the value of my later payments?

The structure typically includes a small, compounding annual percentage increase to help offset standard inflation rates over the course of the payout timeline.Can I sell my future annuity payments for a lump sum later?

While third-party financial companies often offer to buy lottery annuities for pennies on the dollar, the 2026 bylaws contain strict language discouraging predatory buyouts.Do I need a lawyer before I claim my ticket?

Yes. Because the payout is stretched over decades, establishing a trust and working with a fiduciary is critical to protecting your identity and your assets.